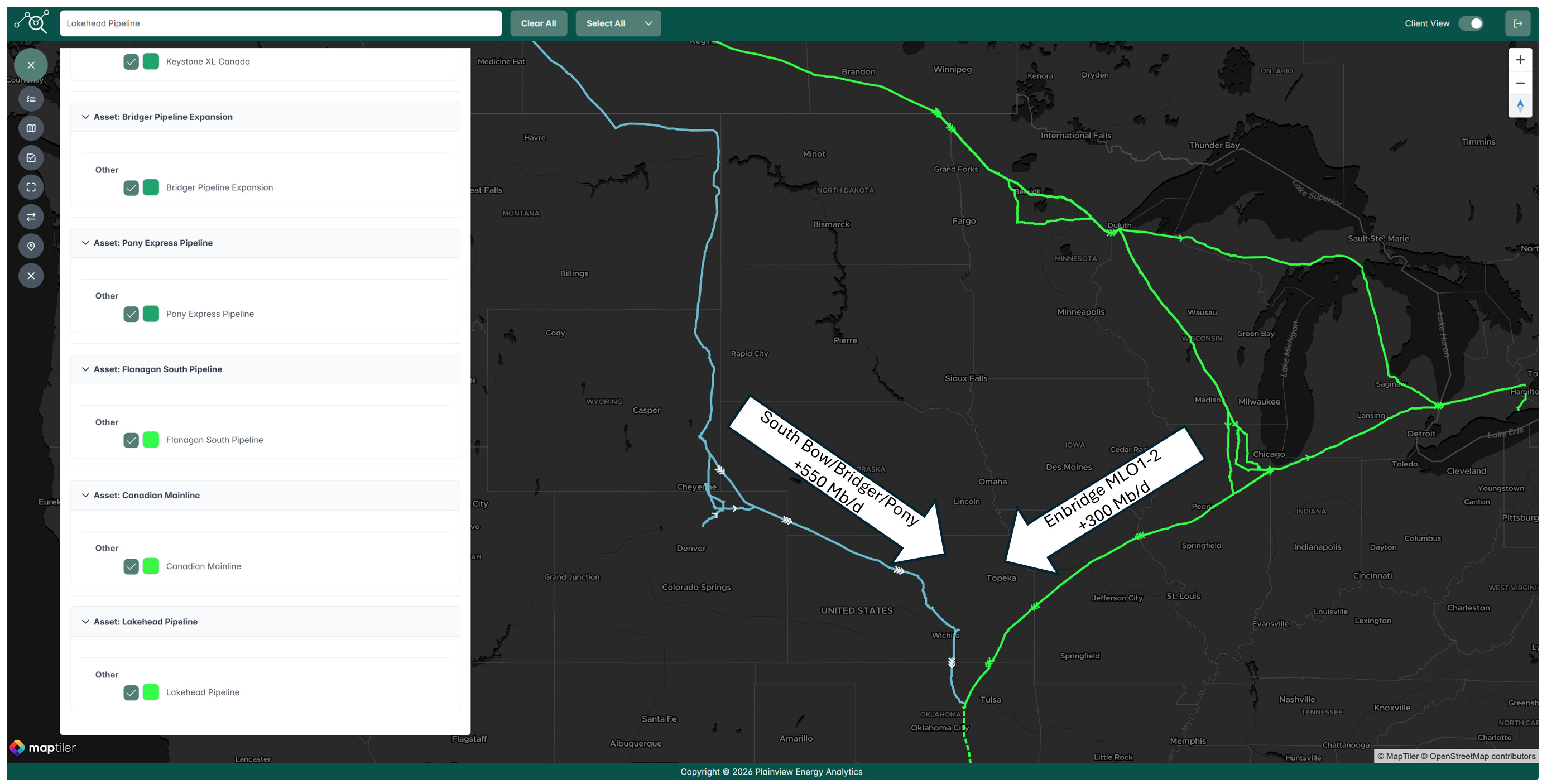

The landscape of Canadian crude oil egress is shifting rapidly with several major “open seasons” and projects proposed over recent months. While much of the industry’s focus has been on moving barrels out of Western Canada, a critical question remains: what happens to this oil once it reaches the U.S. Midwest? With major players like Enbridge (green lines below) and South Bow/Bridger/Pony (blue lines below) proposing multiple expansions, we could see over 850,000 barrels per day (bpd) of new capacity targeting Cushing, Oklahoma, by the end of the decade.

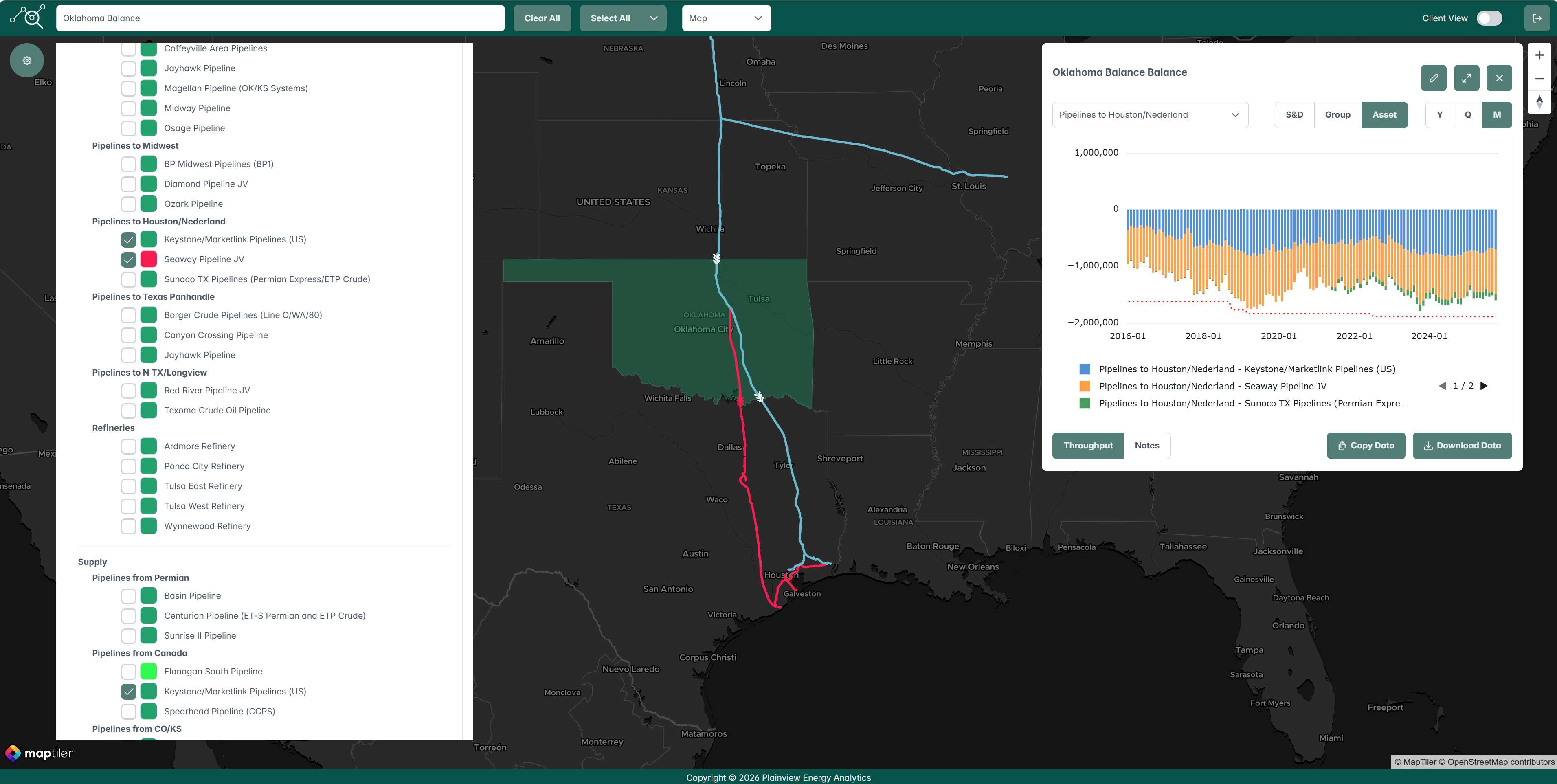

This massive influx of crude raises concerns about potential infrastructure constraints. Historical precedents, such as the 2018–2019 period, show that when the Cushing hub becomes overwhelmed, price dislocations can reach $5 to $6 per barrel compared to Gulf Coast prices. Currently, the primary outlets from Cushing to the Gulf are the Seaway (red line below) and Marketlink (blue line below) pipelines. While both have some latent capacity and expansion potential (roughly 700,000 bpd combined) recent high oil prices could provide enough demand for both the South Bow/Bridger/Pony and Enbridge projects to be sanctioned, which would push Seaway and Marketlink to their absolute limits.

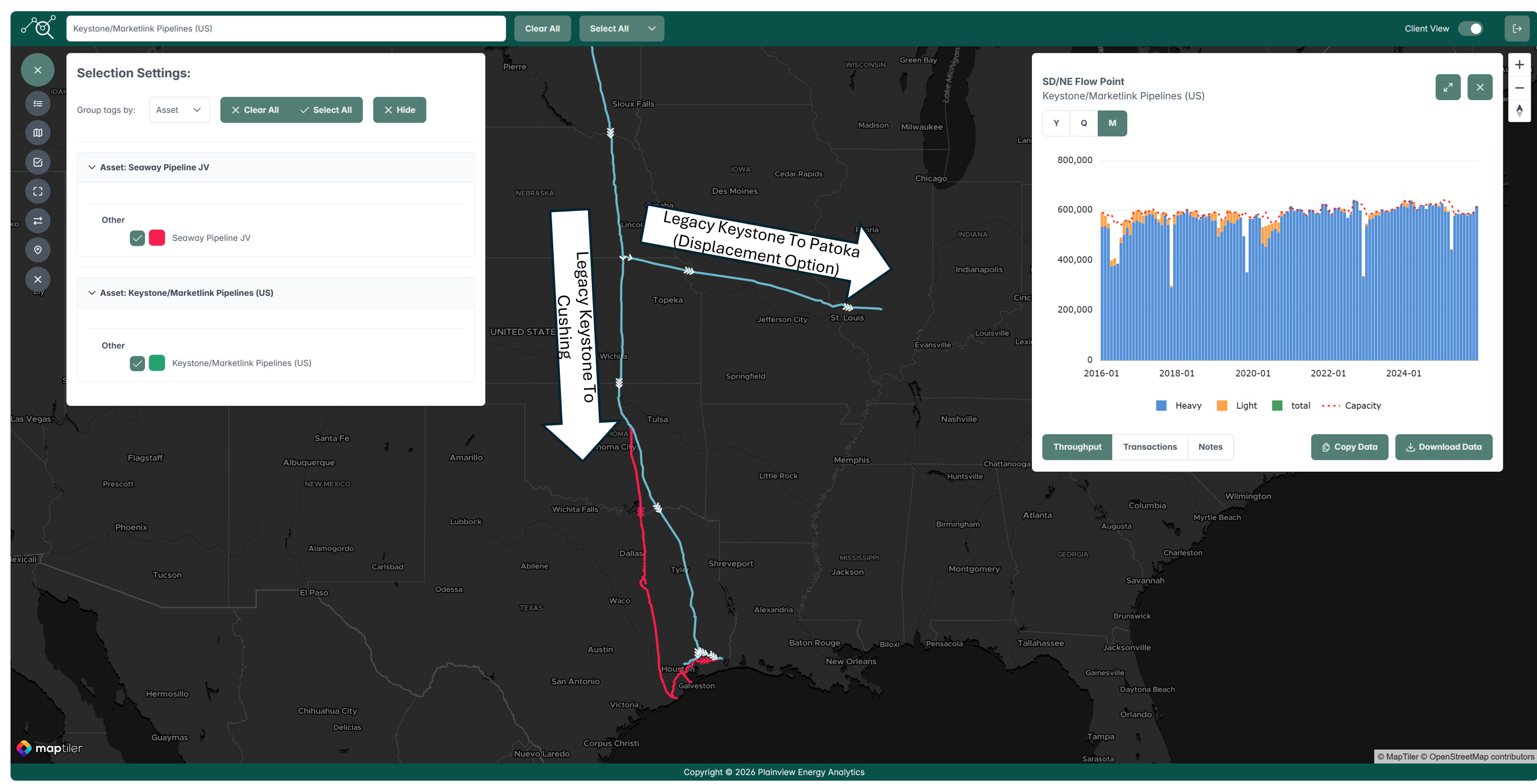

However, the market has built-in mechanisms to prevent a total logjam. As Cushing fills up and prices begin to slightly erode, “displacement” will likely occur. Shippers on Legacy Keystone, for instance, would be incentivized to shift their volumes away from Cushing and toward other hubs like Wood River or Patoka. This rerouting would alleviate pressure on Cushing, effectively “squishing” the barrels toward different markets in search of better pricing.

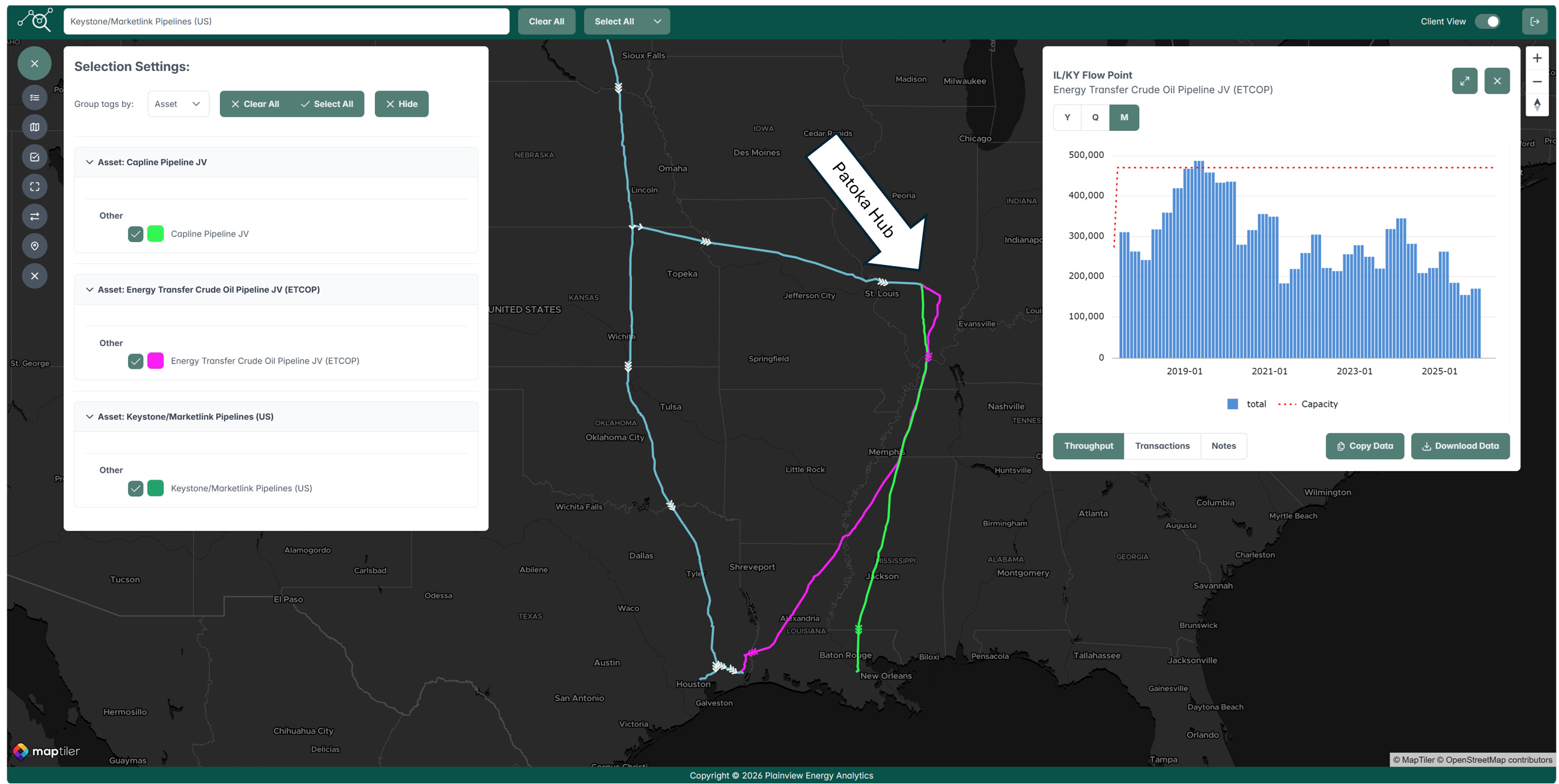

The Patoka hub, in particular, offers a vital safety valve. Pipelines like Energy Transfer’s ETCOP (purple line below) and the Capline system (green line below) currently have significant open space. Capline, a 40-inch pipeline, is easily expandable and could potentially handle over a million barrels per day if necessary. These secondary routes ensure that while Cushing may see some price tightening, the extreme discounts seen in previous years are less likely to recur as the industry utilizes more flexible downstream options.

Special offer for current and future Plainview platform subscribers: Purchase the report from RBN Energy and you’ll receive a dollar-for-dollar credit toward an annual Plainview Platform subscription. This gives you ongoing access to the same interactive flow data, maps, and expanding library of regional supply-demand balances used in the analysis.

The report is now live and can be purchased here:

https://rbnenergy.com/analytics/studies/roundabout