Strait of Hormuz Closure Sends WTI Surging Past $115: Potential 2026 North American Crude Impacts

Backwardation speeds U.S. completions but limits drilling, squeezes refiners, and boosts Permian and midstream pipeline prospects

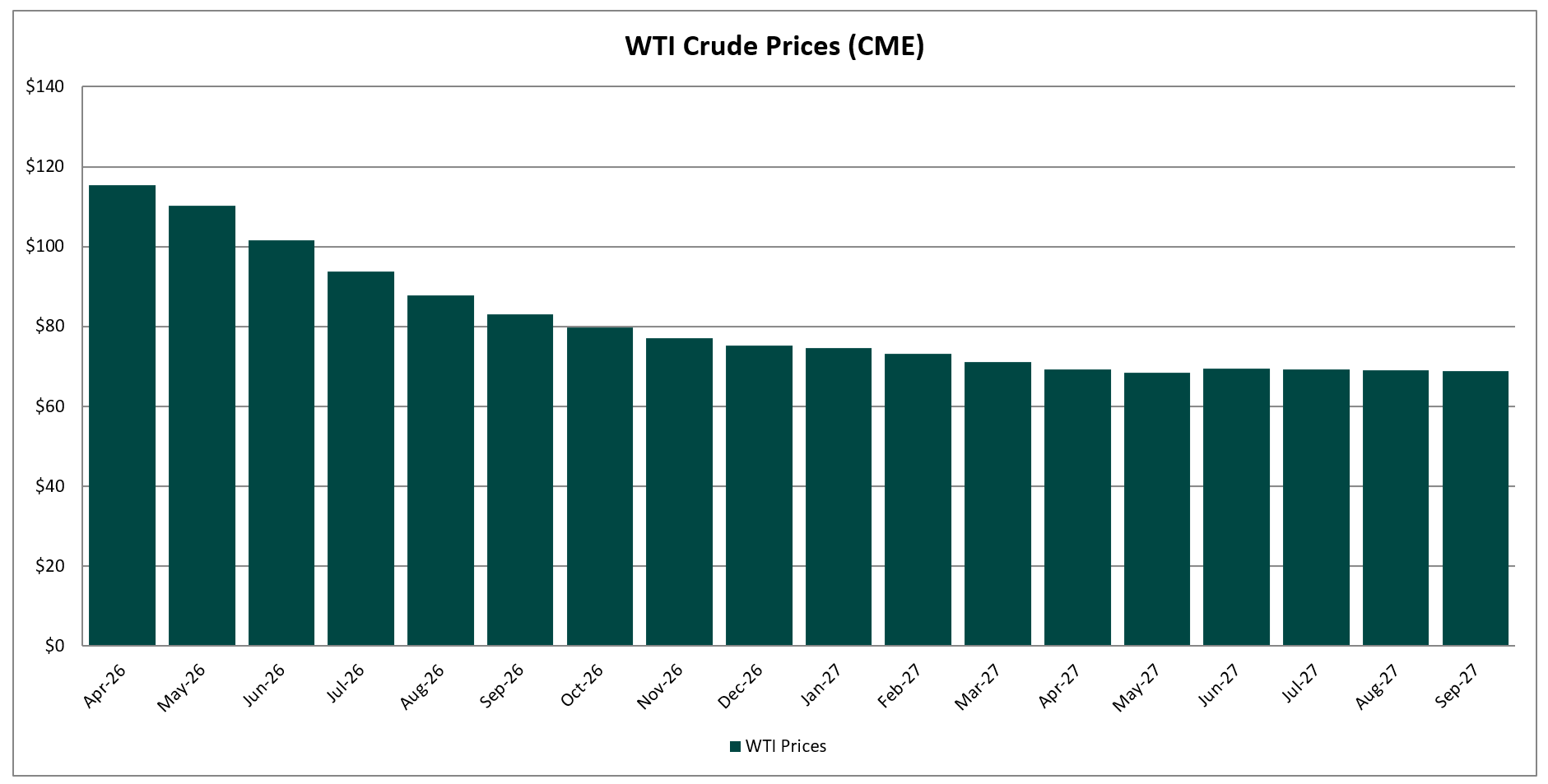

The ongoing conflict with Iran, including joint U.S.-Israeli strikes and Iran’s retaliatory actions, has effectively closed the Strait of Hormuz, disrupting approximately 20% of global crude oil supply through this critical chokepoint. Crude oil prices have relentlessly surged with the futures curve entering extreme backwardation, with near-term April delivery prices hovering around $115 while longer-dated October contracts trade at just $79.

Sky-high near-term prices will prompt U.S. producers to maximize output where possible, accelerating completions by bringing already-drilled wells online sooner and potentially mobilizing additional completion crews. However, the extreme backwardation chills aggressive new drilling, as longer cycle times mean first oil from new spuds would arrive in a much lower-price environment during the second half of 2026. If the current price curve holds, we anticipate mild U.S. production growth (low to mid-single digits percentage) in the near term (spring/summer 2026) through pull-forward efforts, followed by modest medium-term increases (fall/winter 2026) as second-half 2026 forwards average north of $80, supporting selective new activity in tier-1 basins.

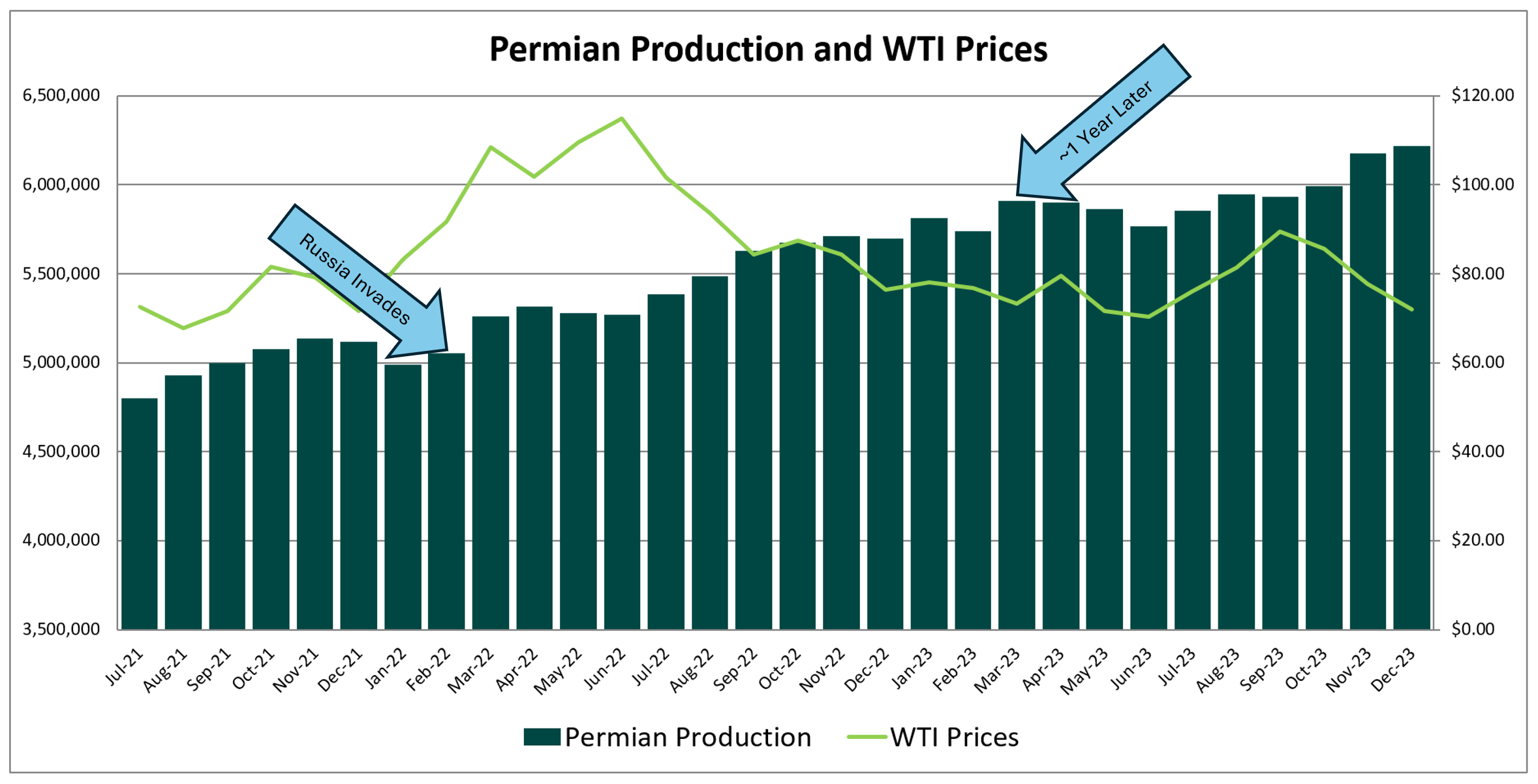

The Permian stands out as the most flexible for ramping production, as demonstrated during the 2022 spike following Russia’s invasion of Ukraine, when it added almost a million barrels per day in a single year. A comparable rapid surge is unlikely under current backwardation, but sustained higher prices in 2H 2026 could substantially boost activity.

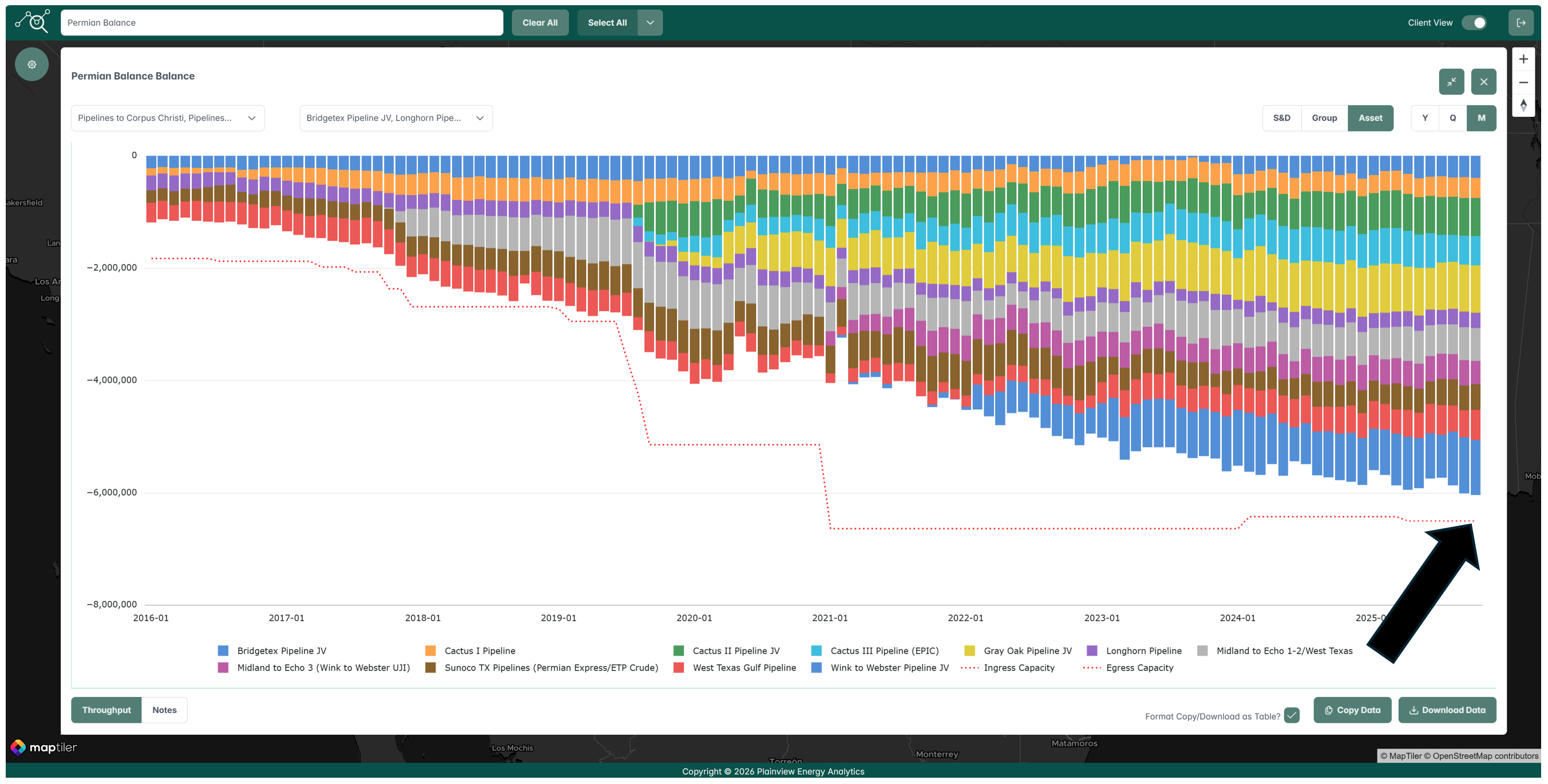

Current data from Plainview’s interactive Permian Basin balance indicates only about 600,000 barrels per day of open crude oil pipeline capacity from the Permian to the Gulf Coast; a meaningful production increase could quickly fill lines, widen basis spreads, and catalyze new expansion projects.

Prolonged high prices would deliver clear benefits to midstream infrastructure via elevated throughput, providing tailwinds for crude egress developments out of Canada, the Rockies, and especially the Permian. The outlook stays highly uncertain, with extreme bullish scenarios (prices potentially exceeding $150 per barrel) or bearish resolutions (dropping below $80) possible by week’s end, depending on geopolitical developments and any U.S. efforts to reopen shipping lanes.

Downstream, global refiners face severe pressure as supply disruptions force demand rationing through elevated prices, potentially cutting worldwide throughput by over 15% and crushing margins. Refineries may reduce runs sharply, with some vulnerable facilities facing temporary idling or curtailments, particularly in regions reliant on disrupted Middle East crudes. While international demand proves more elastic to price shocks, U.S. gasoline consumption would also soften over time as consumers adapt to persistently higher pump prices, further eroding downstream profitability in this volatile scenario.

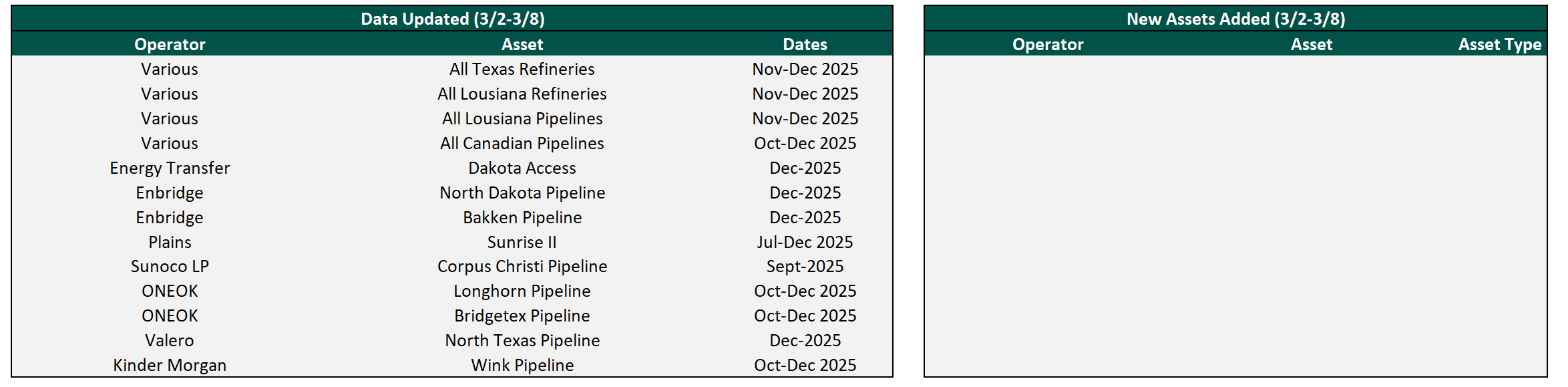

Flow/Transaction Updates and New Assets Under Coverage

Plainview has over 300 assets with crude oil flow or transactional data on our platform and continues to add more each week. Data for existing assets under coverage are posted as soon as they become available. Below are the assets that were updated this week or newly added to coverage.