Hormuz Closure: Widening Spreads Unlock U.S. Crude Pipeline Gains and Possible Rail Revival

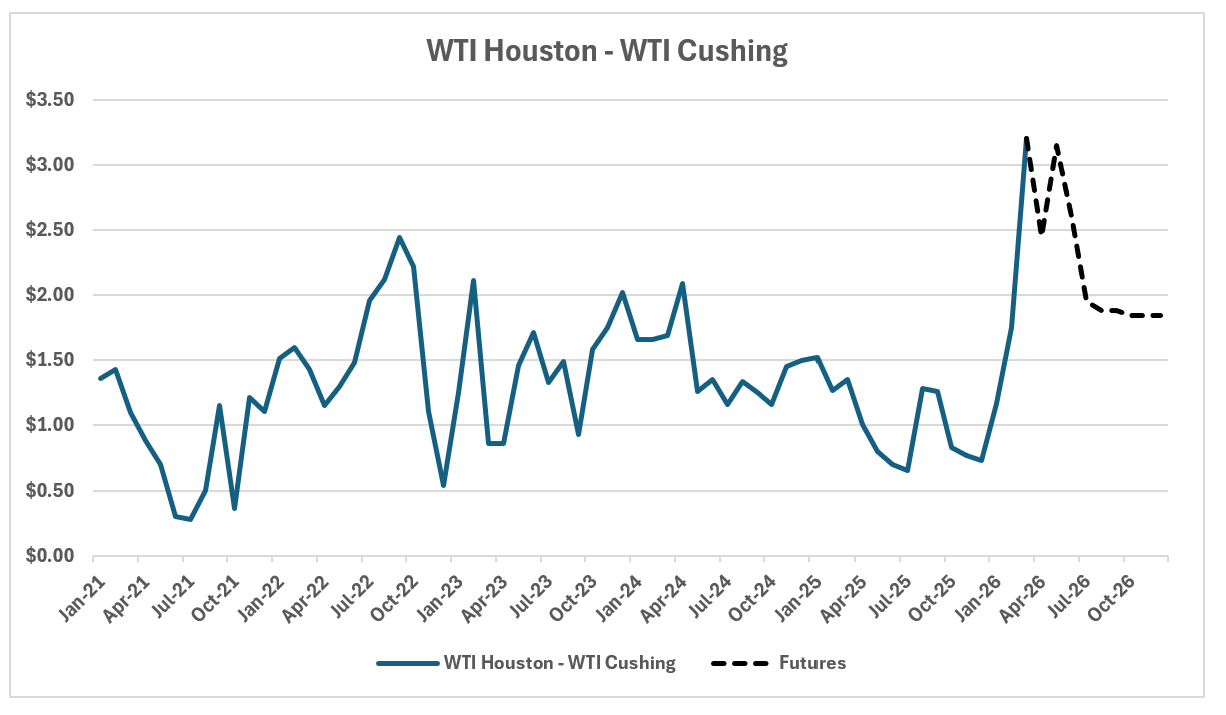

Cushing-Houston Spread ~$3 Signals Full Pipelines and Tariff Upside | Brent-WTI at $12–$14 Boosts Bakken Rail to Coasts

Cushing-Houston WTI Spread Widens: Pipeline Upside for Seaway, Marketlink, and Energy Transfer

The ongoing U.S.-Israel conflict with Iran has led to the effective closure of the Strait of Hormuz, disrupting global seaborne oil flows and causing oil prices to spike sharply. This has triggered a scramble for available open-water barrels, lifting prices for Brent-linked seaborne crude while landlocked U.S. barrels like WTI at Cushing remain relatively discounted. Coastal refineries, competing for scarcer imported supplies, face higher costs for Brent-priced barrels, widening differentials between key U.S. pricing points. Notably, the spread between WTI at Houston and WTI at Cushing, typically depressed post-COVID to $1–$1.50 per barrel due to ample pipeline capacity, has widened significantly to ~$3 per barrel.

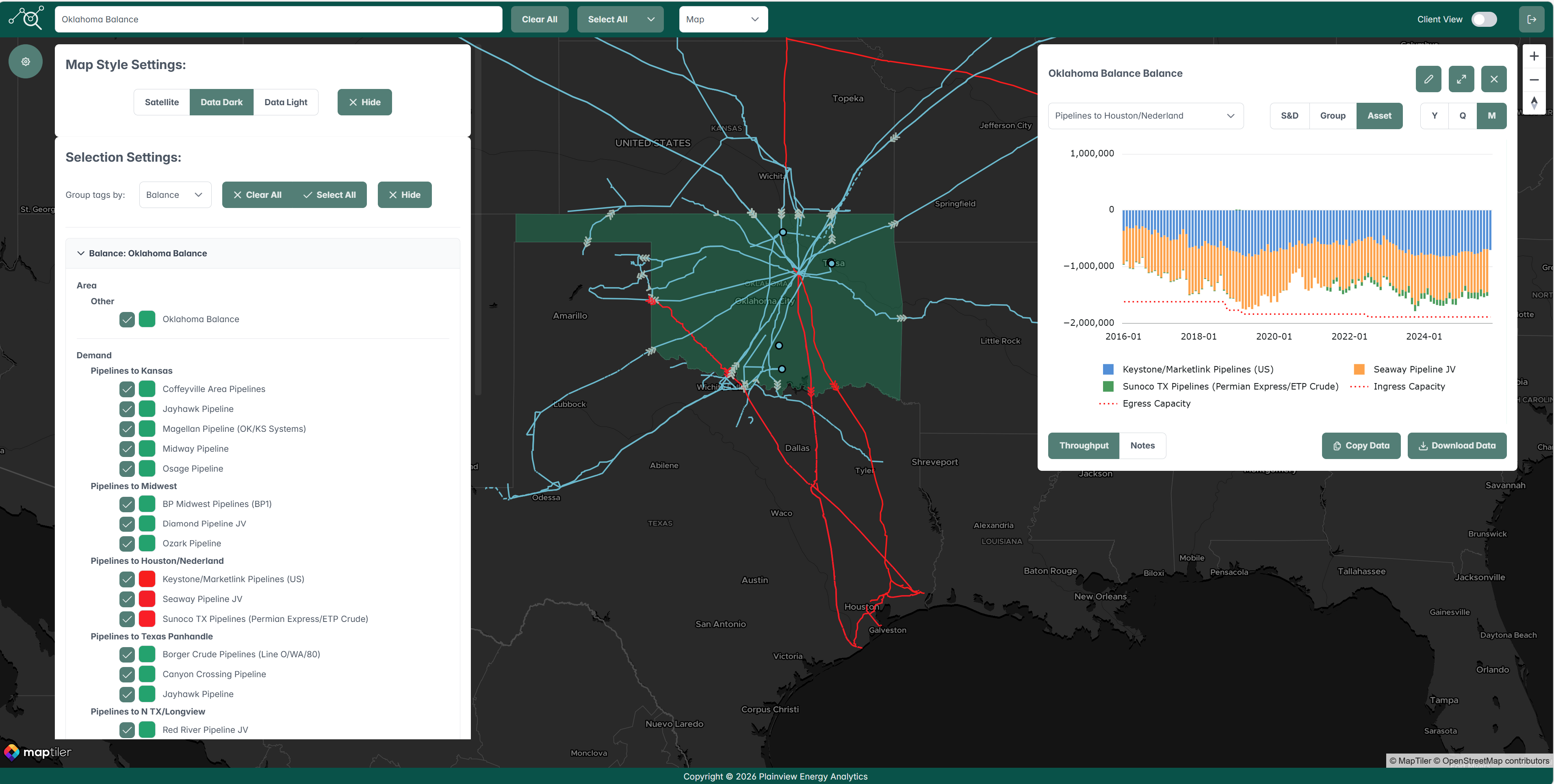

This widening implies strong demand pulling barrels from Cushing toward the Gulf Coast to replace disrupted seaborne imports, likely filling pipelines such as Seaway, Marketlink, and Energy Transfer’s Centurion/Permian Express routes (shown in red below). With current market-based uncommitted tariffs averaging around $1 per barrel, the larger spread suggests these lines are now operating at or near full capacity. If the Hormuz disruption proves long-term, pipelines from Cushing to the Gulf could see substantial upside, enabling operators like Enterprise/Enbridge (via Seaway), South Bow (via Marketlink), and Energy Transfer to potentially increase volumes or raise market-based tariff rates on uncommitted barrels, boosting their economics amid the supply crunch.

Brent-WTI Spread Widens to $13–$14 in 2026 Iran Conflict: Boosting Bakken Crude Rail Shipments to U.S. Coasts?

The widened Brent-WTI spread, now hovering around $13–$14 per barrel amid the ongoing Iran conflict (compared to the typical $3–$5 range), has created a significant discount for WTI-priced U.S. crude. This dynamic encourages North American refiners (particularly those on the coasts) to favor cheaper domestic barrels linked to WTI hubs like Cushing, Guernsey, and Bakken over pricier waterborne imports benchmarked to Brent, which could boost rail shipments as an alternative to seaborne imports.

While several U.S. crude production areas could see an uptick in rail volumes, the Bakken stands out due to its history of substantial rail movements. In 2015, The Wall Street Journal compiled data on crude-by-rail shipments of Bakken crude across the U.S. The map below, though based on 2015 data, illustrates the historic routes these barrels traversed, with prominent paths to both East and West Coast refineries.

Map: Crude Oil Transported by Rail Source: State Emergency Response Commissions

© The Wall Street Journal / Dow Jones & Company, Inc. Published December 3, 2014

https://graphics.wsj.com/crude-oil-by-rail/

Today, about 90% of Bakken rail volumes head to the West Coast and 10% to the East Coast. However, any sustained increase in rail movements faces hurdles: futures markets anticipate a sharp narrowing of the spread to under $6 by mid-2027, complicating efforts to lock in long-term favorable margins. Railroads also lack substantial spare capacity for rapid scaling, requiring time-consuming contracting and planning, challenges amplified by the expected near-term convergence of the spread.

Flow/Transaction Updates and New Assets Under Coverage

Plainview has over 300 assets with crude oil flow or transactional data on our platform and continues to add more each week. Data for existing assets under coverage are posted as soon as they become available. Below are the assets that were updated this week or newly added to coverage.