Global Export Surges and Shifting Crude Spreads: What’s Next for U.S. Midstream Infrastructure?

How geopolitical conflict and massive storage draws triggered temporary bottlenecks, normalized regional price spreads, and set the stage for long-term production growth.

Crude Oil Price Spreads Narrow as U.S. Storage Draws and Pipeline Capacity Stabilize Global Markets

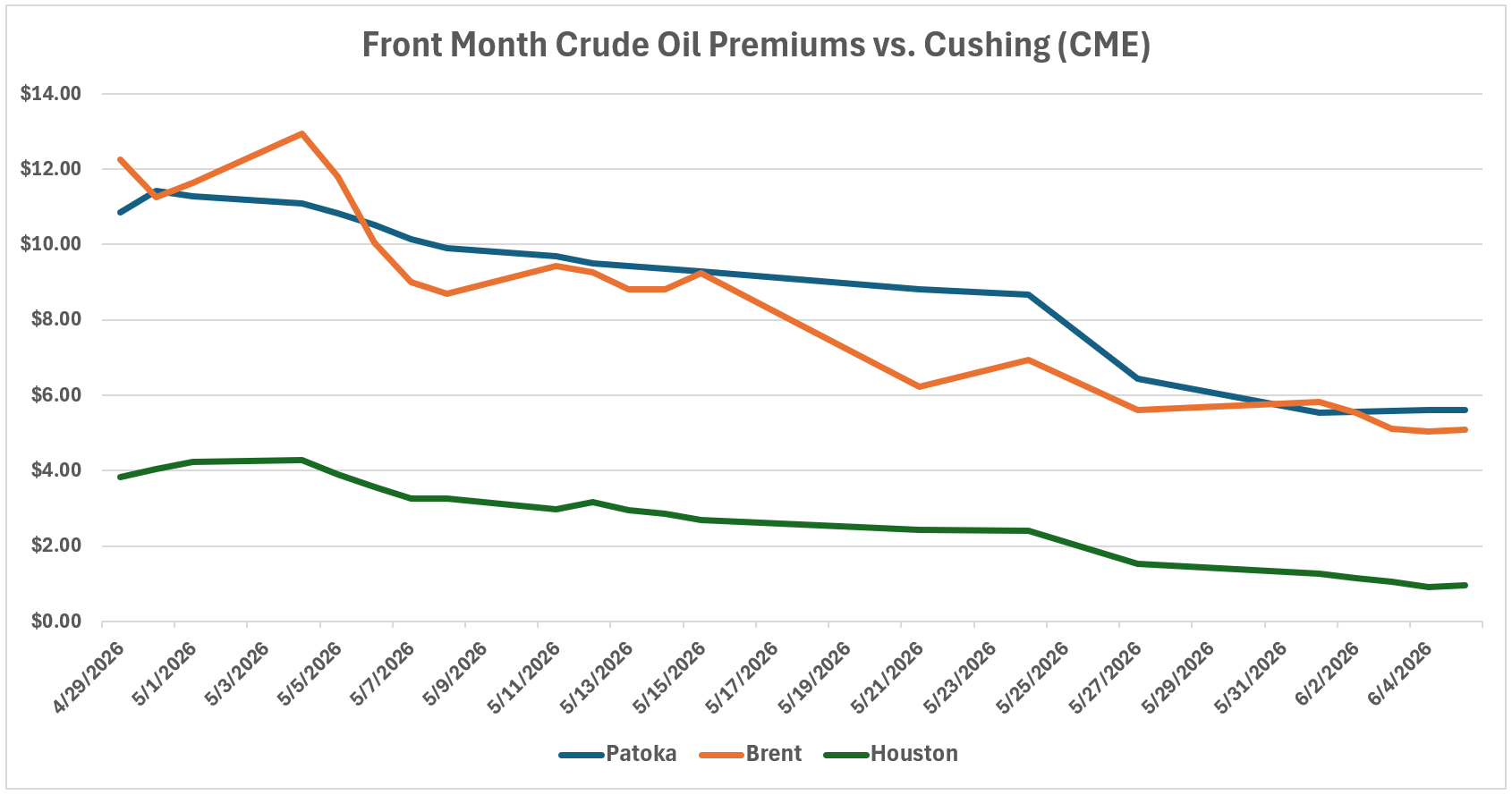

Global energy markets experienced a dramatic shift this spring as regional crude oil price spreads between U.S. and international markets widened significantly, peaking in early May. Driven by the Iran conflict, the Brent to WTI Cushing spread neared $13 per barrel for front-month delivery, while domestic U.S. spreads also spiked. Patoka crude commanded an $11 premium over WTI Cushing, and Houston pricing surged to a premium of over $4. This massive pricing dislocation incentivized a heavy volume of crude oil to drain from both commercial and SPR stockpiles to the international markets. Consequently, the surge in supply has notably normalized prices and narrowed regional spreads. By early June, the Brent/WTI spread has collapsed to around $5, the Patoka premium was cut in half, and Houston pricing reverted to its historical baseline of about $1 over Cushing.

While this storage-driven export boom provided a highly profitable short-term volume bump for U.S. pipelines and terminals, the upside faces a likely expiration date as storage inventories dwindle. Pipeline flows should slowly normalize back to pre-conflict levels in the short-term. However, we view the midstream outlook optimistically longer-term. The rapid depletion of global storage combined with ongoing geopolitical risk should support higher long-term crude prices. Higher sustained prices will inevitably incentivize increased U.S. production, creating a tailwind for healthy, sustainable growth environment for U.S. infrastructure. As long-term production volumes rise, midstream companies can look forward to growing base flows and the distinct potential for future pipeline capacity expansions once existing networks fill back up.

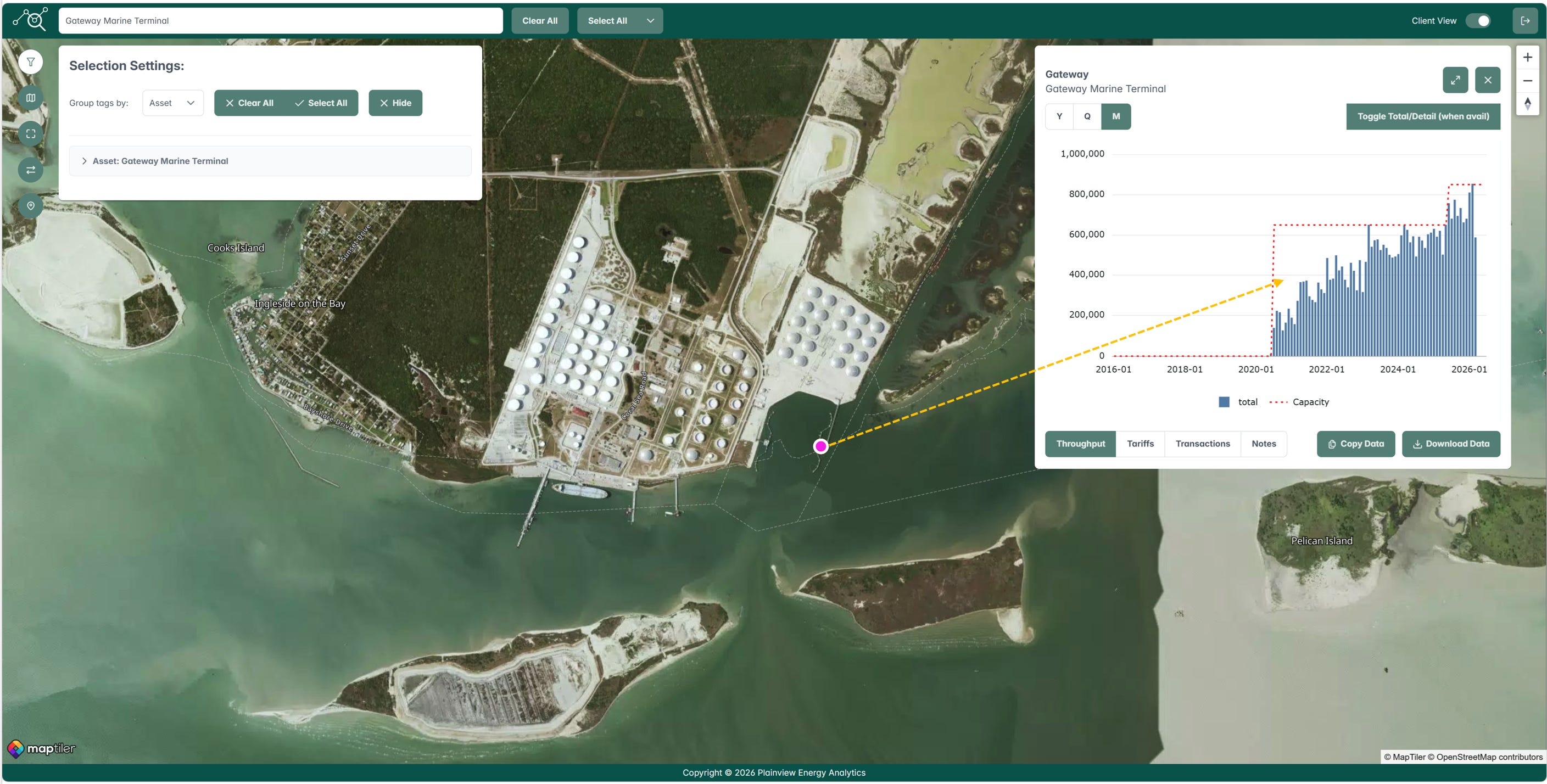

Gibson Energy’s Gateway Terminal Eyes 1M BPD Export Surge After March Slump

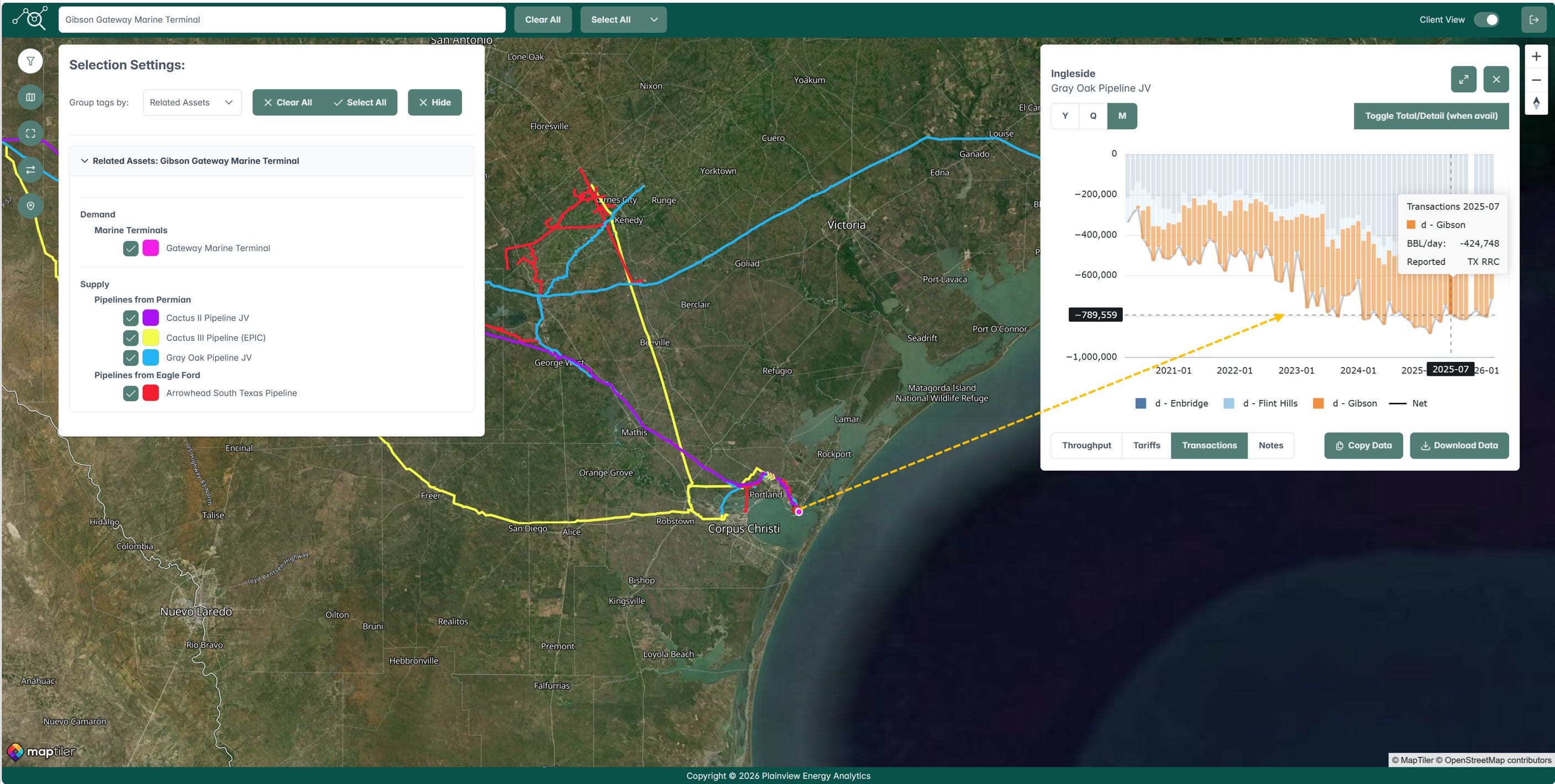

Gibson Energy’s Q1 earnings call highlighted a turbulent start to the year for its flagship Gateway terminal, which faced abrupt export disruptions in March due to shipping bottlenecks and heightened market uncertainty. This operational speedbump was directly reflected in the terminal’s incoming pipeline deliveries, which experienced a sharp contraction, plummeting from a robust average of over 850,000 barrels per day (bpd) in February to just under 600,000 bpd in March (see below). Despite the temporary March drawdown, Gibson Energy projected a rapid recovery for the terminal heading into the latter half of Q2 2026. Management noted on their Q1 earnings call that export volumes are on track to potentially cross the milestone of 1 million bpd, spurred by shifting global logistics and geopolitical tailwinds due to the ongoing Iran conflict.

The Gateway terminal relies on a network of four primary feeder lines: the Eagle Ford-sourced Arrowhead South Texas pipeline managed by Harvest Midstream, and three major Permian baselines, Cactus II, Cactus III, and Gray Oak. The latter two serve as Gibson’s primary volume drivers, with Gray Oak delivering approximately 350,000 bpd and Cactus III contributing around 250,000 bpd based on 2025 baselines (see Gray Oak deliveries to Gibson in below).

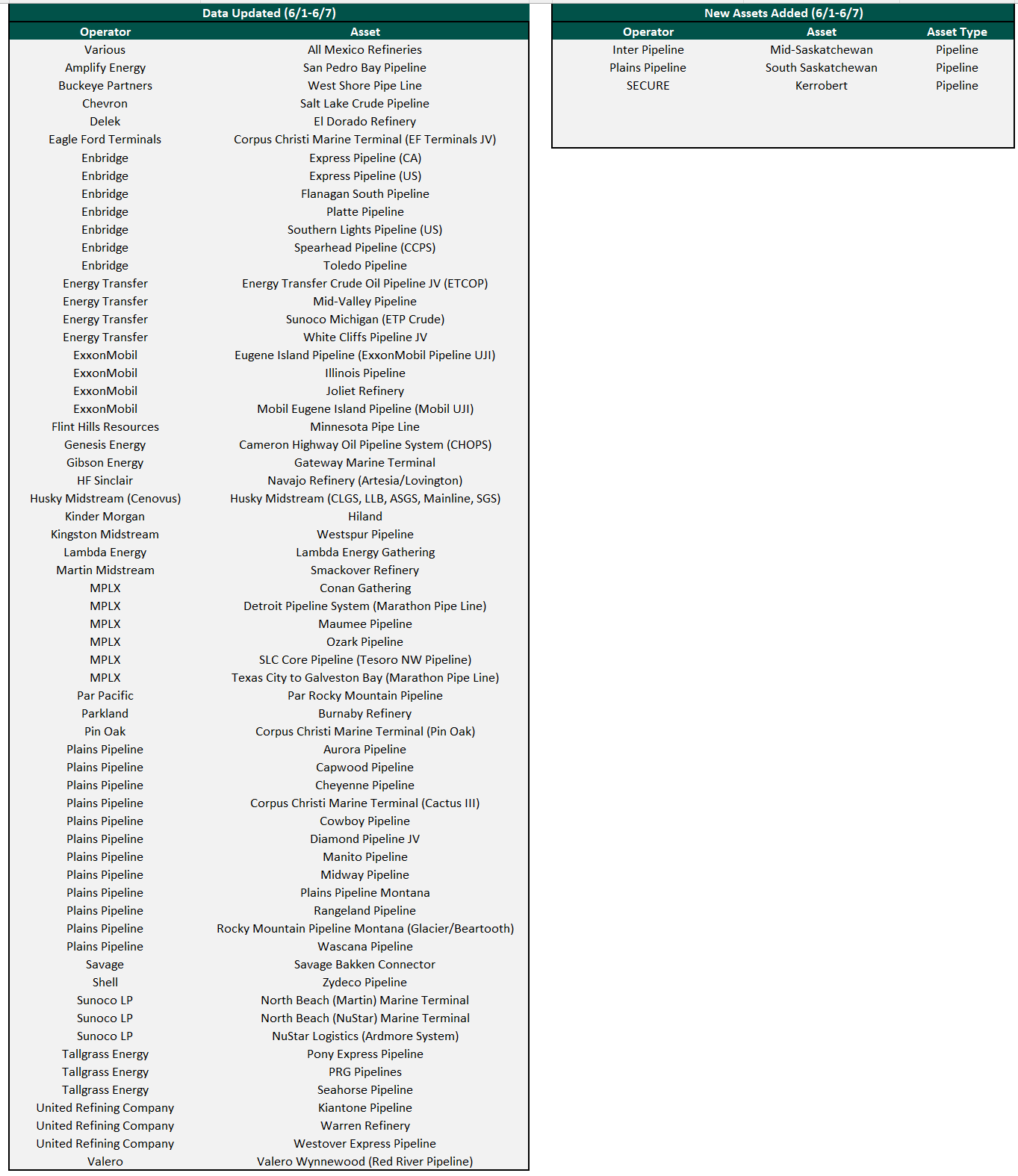

Flow/Transaction Updates and New Assets Under Coverage

Plainview has over 400 assets with crude oil throughput or transactional data on our platform and continues to add more each week. Data for existing assets under coverage are posted as soon as they become available. Below are the assets that were updated this week or newly added to coverage.