Eagle Ford Pipeline Rates Hit Record Lows While Gulf of Mexico Offshore Oil Surges in 2025

Sunoco LP’s East Leg tariff falls to $0.21/bbl amid basin overcapacity; Shenandoah and Whale drive 200,000+ b/d Texas pipeline gains

Record Low $0.21/bbl Rate: NuStar’s New Tiered Tariff Targets Higher Volumes in Eagle Ford

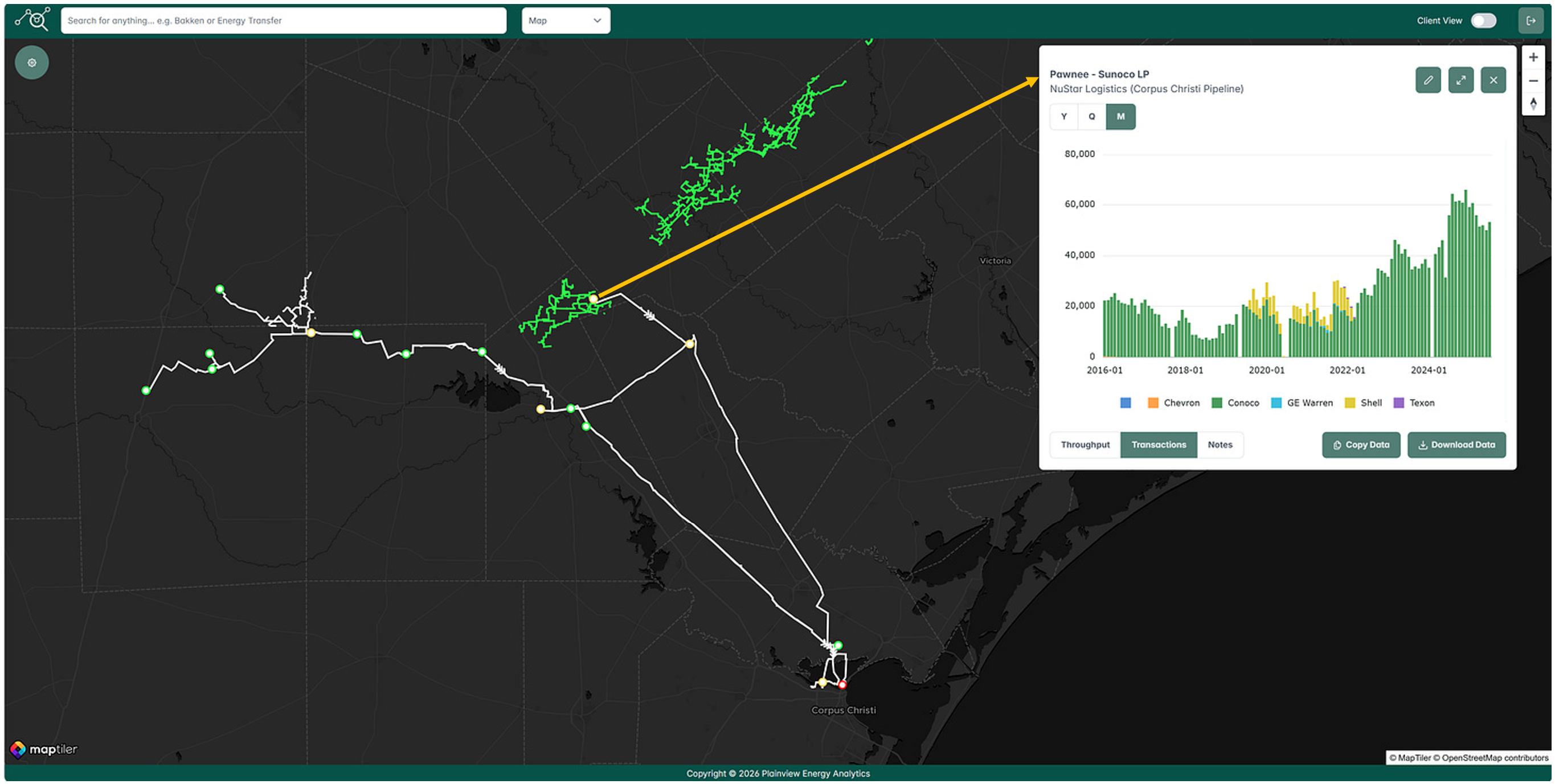

NuStar Logistics (owned by Sunoco LP) recently filed a new tariff for its East Leg South Texas crude line (the far east white line in the map below), which transports Eagle Ford crude from the Pawnee Terminal (orange arrow) to terminals in Corpus Christi. Originating in the heart of the Eagle Ford shale play, this line introduces a temporary incentive-based rate structure aimed at encouraging higher volumes.

Shippers committing to a minimum of 26,000 barrels per day over a three-year term can access tiered rates: approximately $0.40 per barrel for volumes up to 65,000 barrels per day, dropping to ~$0.21 per barrel for any volumes exceeding 65,000 barrels per day. The Pawnee Terminal ties into ConocoPhillips’ crude gathering system (green lines), which has been used exclusively by Conoco for the past three years. This discounted structure likely stems from an agreement to incentivize additional shipments from that producer.

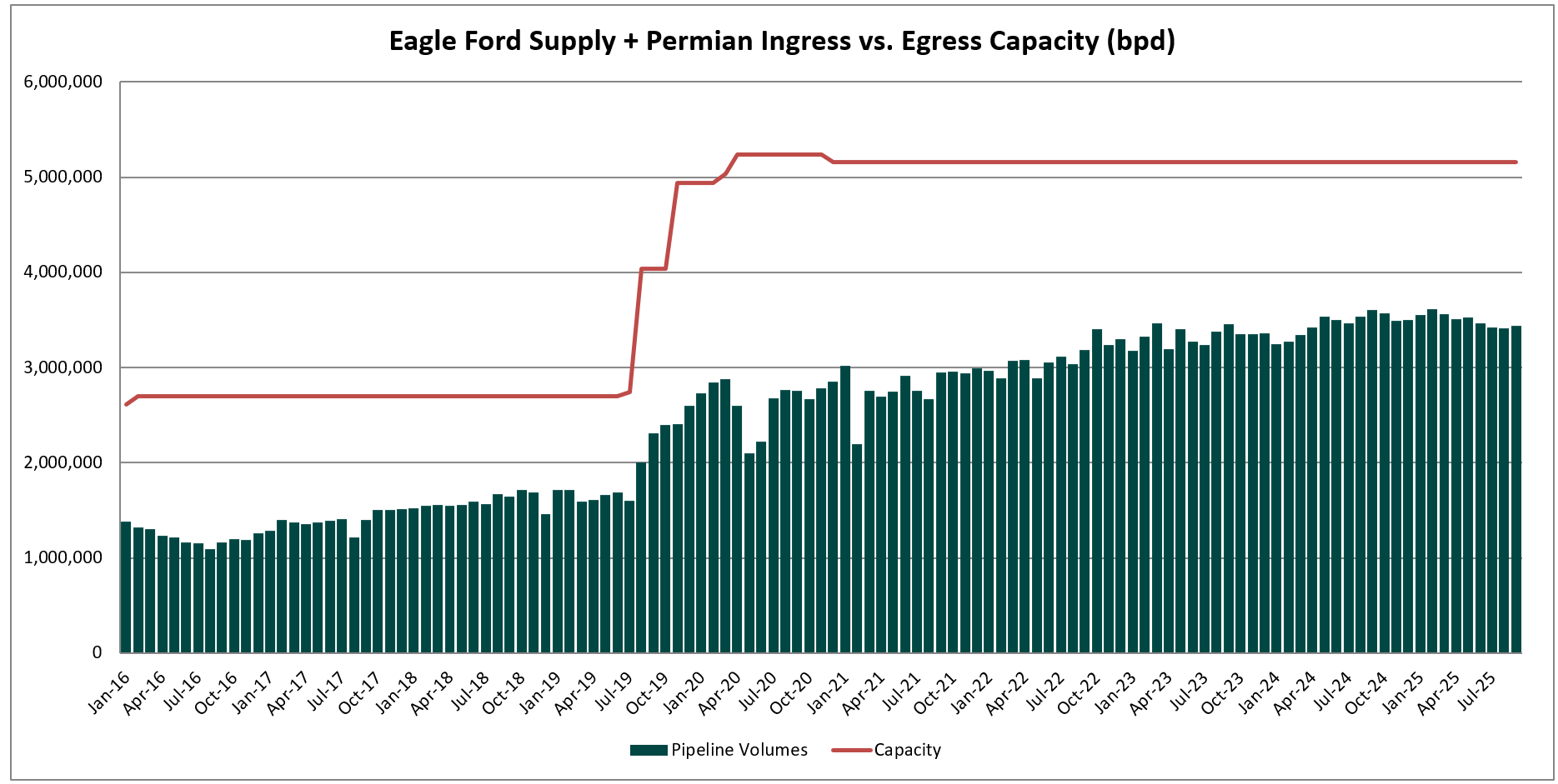

This tiered approach, common in overbuilt pipeline regions, allows pipelines to secure higher rates on lower volumes while incentivizing producers to reduce their average transportation costs through increased throughput. The $0.40/$0.21 per barrel tiered rate structure marks one of the lowest ever seen for Eagle Ford egress pipelines and represents an 80 percent cut from the original contract rates, which ended in 2023 at $1.81/$1.13 per barrel, underscoring the challenges of severe overcapacity in the basin.

Eagle Ford crude egress capacity now exceeds 5 million barrels per day, including lines that also carry Permian volumes to Corpus Christi, resulting in roughly 2 million barrels per day of excess capacity dedicated to local Eagle Ford production. This situation serves as a cautionary example of how pipeline overbuilds can drive aggressive pricing to fill underutilized infrastructure.

Gulf of Mexico Offshore Oil Surges 10%+ in 2025: Texas Pipelines Gain Share as Shenandoah and Whale Boost Volumes

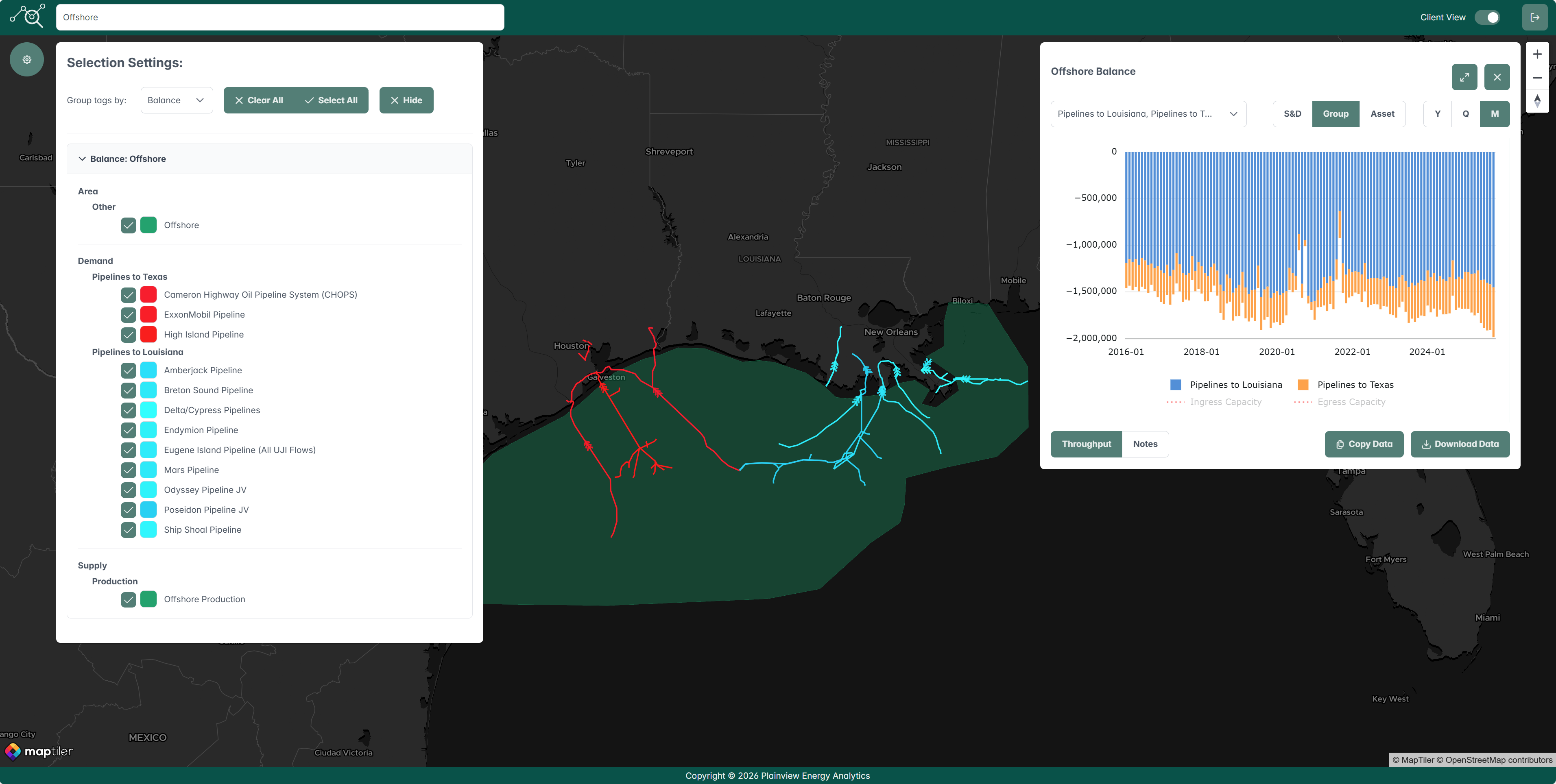

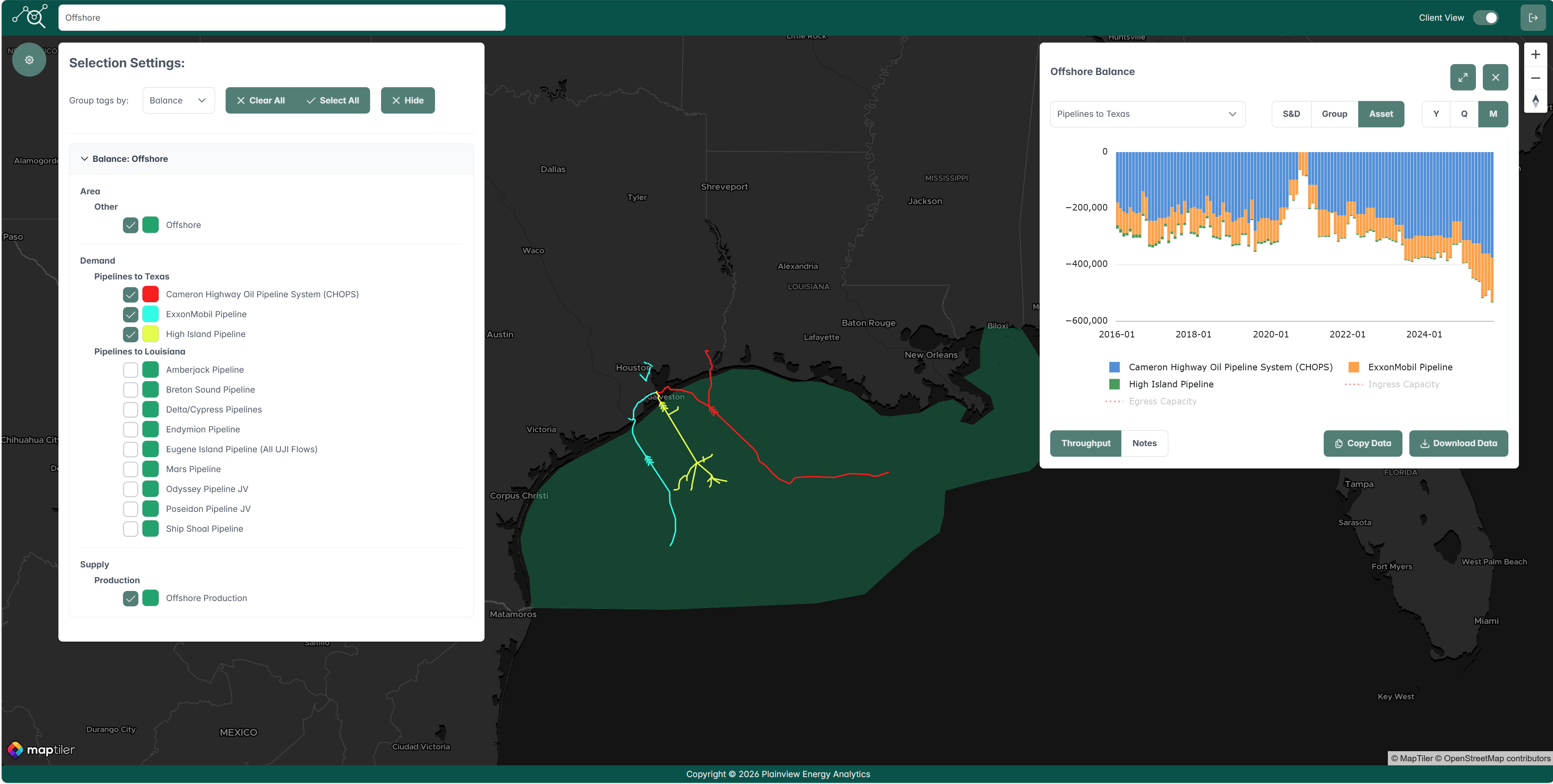

Offshore production in the Gulf of Mexico remains a strong driver of U.S. oil growth in 2025, with volumes rising more than 200,000 barrels per day compared to 2024, representing over 10 percent growth. A significant portion of this increase has been directed to pipelines transporting crude to Texas destinations (red pipelines in map below), enabling those routes to capture greater market share from Louisiana-bound systems (blue pipelines).

Key contributors include the Shenandoah platform, which began production in July 2025 and has boosted volumes on the Genesis-operated CHOPS (Cameron Highway Oil Pipeline System - red pipeline in map below) by over 60,000 barrels per day year-over-year. This builds on earlier gains from the Argos and Mad Dog 2 projects that came online in 2023 and also fed into CHOPS. Additional momentum comes from ExxonMobil’s HOOPS (Hoover Offshore Oil Pipeline System - blue pipeline), which has seen substantial volume growth in 2025 following the Whale project’s startup in early 2025, adding more than 70,000 barrels per day to flows.

Combined, these major offshore developments feeding Texas-bound pipelines have increased throughput by over 100,000 barrels per day compared to the prior year, highlighting the Gulf’s role in sustaining production momentum amid new deepwater tie-ins and expansions.

Flow/Transaction Updates and New Assets Under Coverage

Plainview has over 300 assets with crude oil flow or transactional data on our platform and continues to add more each week. Data for existing assets under coverage are posted as soon as they become available. Below are the assets that were updated this week or newly added to coverage.