Don’t Buy the Hype: What Cushing Tank Bottoms Really Mean for Oil Prices

Inside Oklahoma's Crude Oil Balance: How 28 pipelines protect WTI Cushing from exponential price spikes even at 20 million barrels.

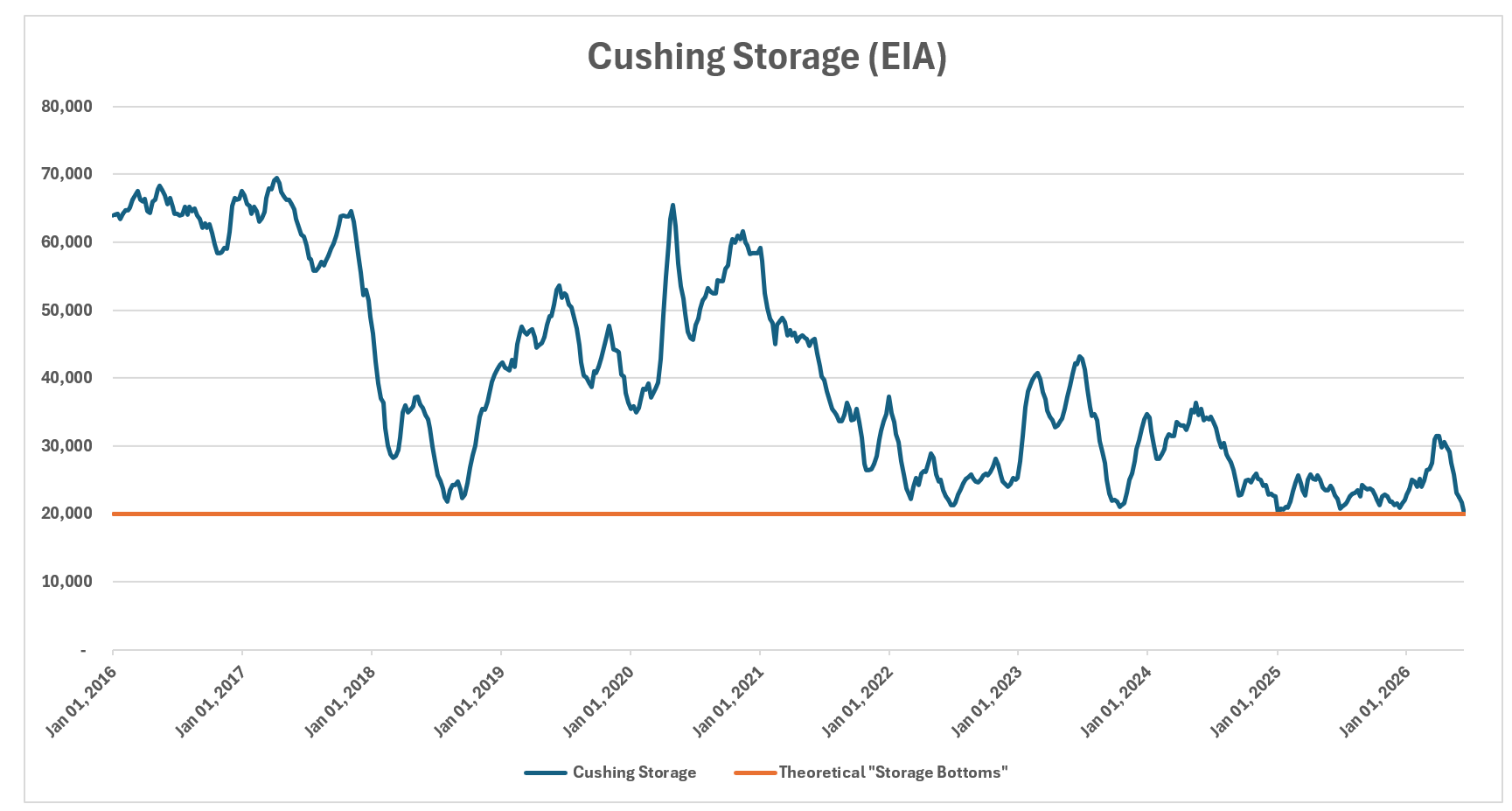

Recent discussions across the oil markets have centered on Cushing storage volumes hitting “tank bottoms” after the Iranian conflict pulled significant volumes from the hub. The Energy Information Administration (EIA) recently reported that as of mid-June 2026, storage volumes at Cushing dropped to 20 million barrels, a level historically recognized as the operational bottom (see graph below). Below this point, storage operators and refiners have historically become highly reluctant to sell their barrels due to inventory risk and potential operational issues at storage facilities. While this low inventory level is frequently used to fuel an ultra-bullish market narrative, the belief that low Cushing inventories will trigger an extreme rise in crude oil prices stems from a fundamental misunderstanding of the hub’s global connectivity and spare pipeline capacity.

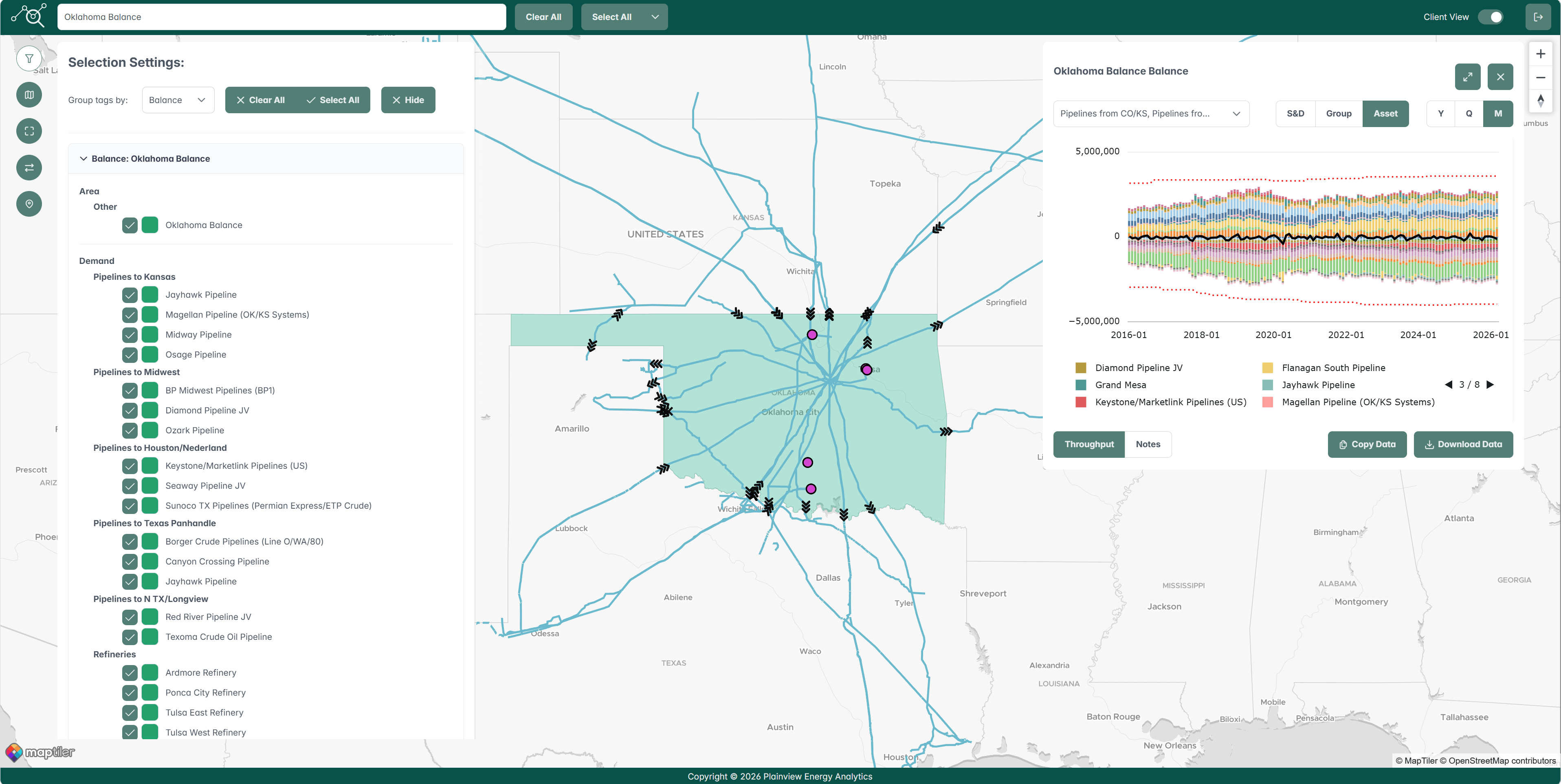

As arguably the most well-plumbed inland storage hub in the world, Cushing is connected to numerous U.S. oil hubs and the Gulf Coast via more than two dozen pipelines. Plainview’s crude oil platform monitors flows and capacities on 28 pipelines in and out of Oklahoma, throughputs in the state’s five refineries, storage balances, and in-state oil production to form our “Oklahoma Balance” which is updated monthly (see figure below). This extensive infrastructure allows the Cushing hub to seamlessly balance its own market dynamics. During periods of oversupply, excess crude is pushed out to Gulf export facilities, while in times of relative undersupply, those same pipelines simply reduce the volume of barrels leaving the hub to stabilize local inventory.

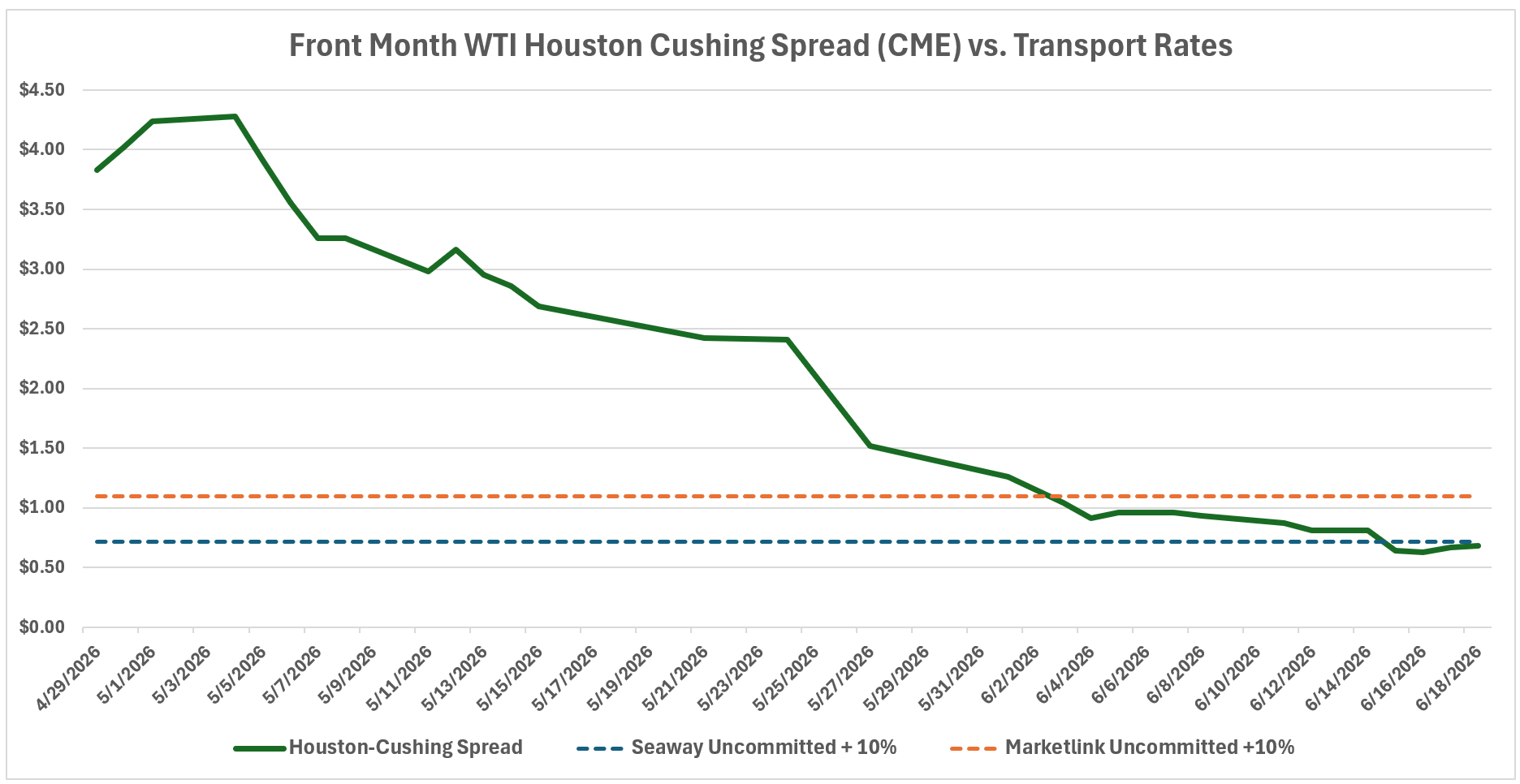

Because of this built-in flexibility, tight inventory is primarily impacting price spreads between major U.S. hubs rather than driving outright WTI crude prices higher. The spread between Cushing and Houston, which peaked above $4.00 in early May as barrels rushed to the Gulf Coast for export, has narrowed drastically to under $0.70 a barrel. At this sub-$0.70 level, it is no longer economically viable to ship uncommitted barrels from Cushing to the Gulf Coast on pipelines like Seaway or Marketlink (see graph below). This narrowing spread indicates that Cushing is already successfully pricing its crude to retain barrels locally, likely bringing an end to the heavy inventory draws seen throughout May and the first half of June. While major geopolitical events can always trigger much higher worldwide prices, a tight Cushing market simply prices itself to trade near historically stronger benchmarks like Houston and Brent to keep its barrels from leaving, rather than massively lifting the entire global complex.

Flow/Transaction Updates and New Assets Under Coverage

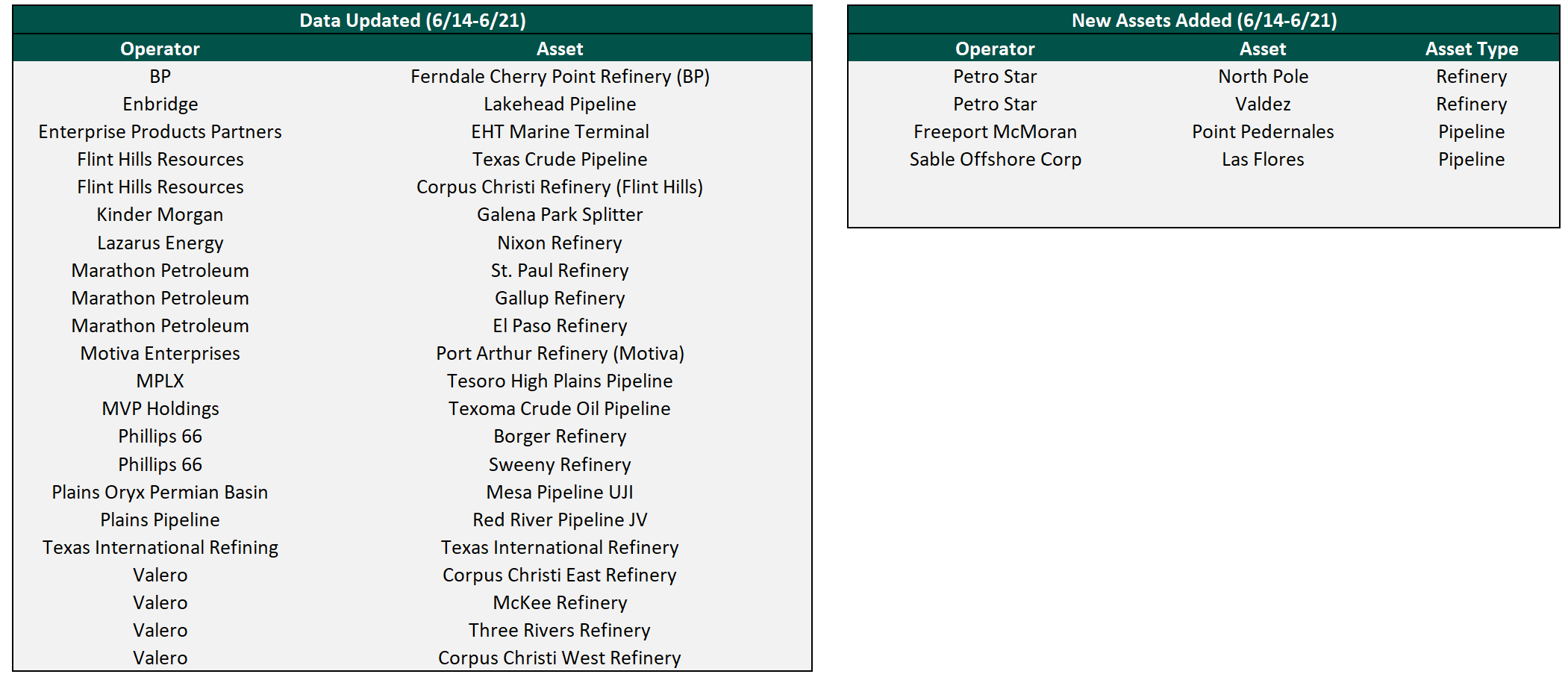

Plainview has over 400 assets with crude oil throughput or transactional data on our platform and continues to add more each week. Data for existing assets under coverage are posted as soon as they become available. Below are the assets that were updated this week or newly added to coverage.

Cushing cannot raise the global price itself. But if US export machine is the buffer on the supply shock, certainly Cushing (and other US hubs) self-regulating to stop export is an indirect pressure on global price.

I get you that it's not a silver bullet. But Brent flows are still majority force majeure'd, so surely the implication of Cushing low inventory raising prices, if indirect, still holds true until we see Hormuz back up to 10 mbpd?

Or am totally wrong?

So if Cushing re-prices itself to other benchmarks, in order to not fall below operational minimums, what does that mean for a world starving for supply? Don't the other benchmarks just start soaring once Cushing re-prices itself in a way that denies export?

I get the idea of Cushing regulating it's own supply and that it probably won't fall below a certain supply. But that regulation of supply means the indirect effect will hit demand, via price mechanisms, right? How else do you avoid shortage, especially in a world where Brent is a hypothetical input until the Strait fully normalizes?

I'm not fully getting the article because you deny shortages and price increases, however the mechanism you describe, regulates shortages via price increases. Maybe I'm missing something.